Note: The information in this guide is for general educational purposes. Mortgage products, rates, and eligibility criteria change weekly and monthly. Always seek advice from an FCA-regulated mortgage adviser (BM14 Finance) before making any financial decisions.

Buying a home is one of the biggest financial decisions most people make in their lifetime and the mortgage application process is the part that trips most people up. Not because it is impossibly complex, but because nobody explains it clearly from start to end.

This guide does exactly that. If you are a first-time buyer just getting started, someone moving up the property ladder, or looking to remortgage, this is everything you need to know about the UK mortgage application process, from your very first affordability check all the way to collecting your keys.

What is the UK Mortgage Application Process?

The mortgage application process in the UK is the series of steps a lender takes to assess whether you are eligible to borrow money to purchase a property. It involves checking your income, credit history, spending habits, and the property itself before a formal mortgage offer is made.

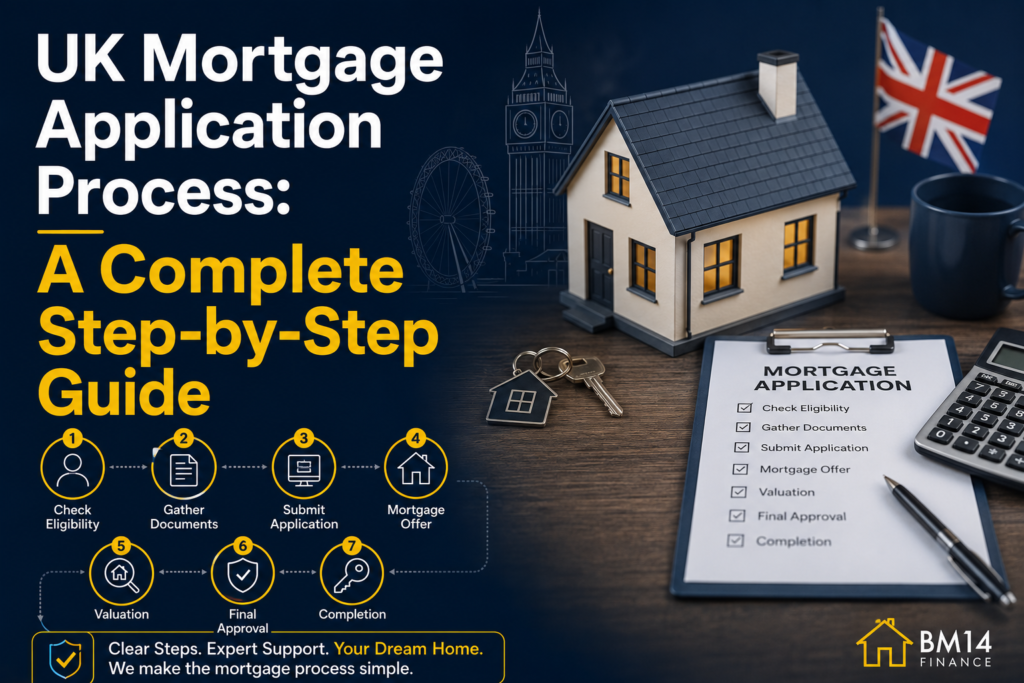

The full process moves through these stages: financial preparation, Agreement in Principle, full application, underwriting, property valuation, mortgage offer, and finally completion. Each stage has its own requirements, timelines, and potential sticking points, all of which are covered in this guide.

How Long Does a Mortgage Application Take?

One of the most searched questions around this topic is how long does a mortgage application take and the answer is: it depends.

For a simple application with all documents in order, the process from full application to mortgage offer usually takes 4 to 6 weeks. However, the complete journey from first talking to a lender to getting your keys can take anywhere from 2 to 6 months, depending on the chain, your solicitor, and the lender’s workload.

UK Mortgage Application Timeline: Stage by Stage

| Stage | Estimated Time |

| Agreement in Principle | Same day to 24 hours |

| Document preparation | 1–7 days (depending on readiness) |

| Full application submission | 1–3 days |

| Underwriting and affordability assessment | 1–2 weeks |

| Property valuation | 3–7 days after instruction |

| Formal mortgage offer issued | 2–4 weeks from full application |

| Conveyancing and completion | 4–12 weeks after offer |

What Can Delay a Mortgage Application?

Most delays are avoidable. The most common reasons a mortgage application takes longer than expected are:

- Missing or incorrect documents, the single biggest cause of delays.

- Lender backlog, busy periods (spring and autumn) slow down underwriting teams.

- Property valuation issues, if the surveyor flags structural problems or down-values the property.

- Solicitor delays, conveyancing timelines vary significantly between firms.

- Additional information requests, lenders may ask for further evidence during underwriting.

- Chain complications, if another buyer or seller in your chain pulls out.

Understanding these pressure points in advance puts you in a much stronger position to avoid them.

Step 1: Get Your Finances in Order Before You Apply

Before you even approach a lender, your financial health matters enormously. Lenders are not just looking at how much you earn, they are looking at how responsibly you manage what you already have.

How Much Can You Borrow?

Most UK mortgage lenders offer between 4 to 4.5 times your gross annual income. Some lenders, particularly for first-time buyers or professionals in stable careers, will stretch to 5 or even 5.5 times income for the right applicant.

For example, if you earn £40,000 a year, most lenders would consider lending between £160,000 and £180,000. At 5.5 times income, that figure rises to £220,000.

Your actual borrowing limit also depends on your existing financial commitments, monthly outgoings, and the size of your deposit.

Tip: Use a mortgage overpayment calculator alongside your affordability figures to understand how making extra payments early in your term could save you thousands in interest over the life of the mortgage.

How Your Credit Score Affects Your Mortgage

Your credit score is one of the first things any lender will assess. A strong credit score does not guarantee mortgage approval, but a poor one can significantly limit your options or push you toward higher interest rates. Before applying, check your credit report through a free service such as ClearScore (Equifax data) or TotallyMoney (TransUnion data).

Common credit score issues that affect mortgage applications:

- Missed or late payments on bills, credit cards, or loans.

- High credit card utilisation.

- Payday loan history (a major red flag for most lenders, even if fully repaid).

- No credit history at all, brokers cannot assess what they cannot see.

- Multiple hard credit searches in a short period.

Key point: Getting a mortgage in principle (AIP) uses a soft credit search, which does not affect your credit score. A full mortgage application triggers a hard search, which does leave a mark. Knowing this distinction helps you shop around without accidentally damaging your credit profile.

How Much Deposit Do You Need?

The minimum deposit for a UK mortgage is 5% of the property purchase price. However, the size of your deposit directly affects the interest rate you are offered.

| Deposit Size | Loan-to-Value (LTV) | Typical Rate Impact |

| 5% | 95% LTV | Higher rates, limited lender choice |

| 10% | 90% LTV | More lenders available |

| 15% | 85% LTV | Noticeably better rates |

| 25%+ | 75% LTV or below | Best rates on the market |

In 2026, UK mortgage rates have been falling gradually following Bank of England base rate adjustments. Some brokers have already seen UK mortgage rates fall below 5% for borrowers with larger deposits, marking a significant shift from the highs seen in recent years. Checking Nationwide mortgage rates alongside other high street lenders and specialist brokers gives you a useful market benchmark before you commit to any deal.

First-time buyers: You may not need to pay stamp duty at all. Many people ask do first-time buyers pay stamp duty? Well, first-time buyers do not pay stamp duty on properties up to £425,000 (subject to current government thresholds, always verify this with your solicitor before completion as thresholds can change). For properties above this threshold, a reduced rate applies up to £625,000.

Step 2: Get a Mortgage in Principle (Agreement in Principle)

Before you start seriously viewing properties, getting a mortgage in principle, also called an Agreement in Principle (AIP), Decision in Principle (DIP), or Mortgage in Principle (MIP) is one of the most important early steps.

What is a Mortgage in Principle?

A mortgage in principle is a conditional statement from a lender indicating how much they would be willing to lend you, based on the financial information you provide. It is not a guarantee of a mortgage offer, but it gives you a reliable borrowing figure to work with when house hunting.

Estate agents will often ask if you have an AIP before arranging viewings. Having one signals that you are a serious buyer, not just browsing and can strengthen your position when making an offer on a property, particularly in a competitive market.

Is a Mortgage in Principle the Same as Pre-Approval?

This is a question many people search for. In the UK, there is no formal “pre-approval” stage in the same way it exists in other countries. What UK buyers refer to when they say mortgage pre-approval is essentially the same as an Agreement in Principle. The two terms are used interchangeably in common conversation, but officially, UK lenders issue AIPs, not pre-approvals.

How Long is a Mortgage in Principle Valid?

Most mortgage in principle offers are valid for 60 to 90 days. If your property search takes longer than this, you can usually renew it. Be aware that some lenders carry out a hard credit search for an AIP (though many use a soft search), so check before applying.

Step 3: Gather Your Documents

Poor document preparation is the most common reason mortgage applications are delayed. Getting everything together before you apply, rather than scrambling once the process has started, can shave weeks off your timeline.

How Many Payslips Do You Need for a Mortgage?

The number of payslips required depends on how often you are paid and the nature of your employment.

| Employment Type | Payslips Required |

| Monthly paid (permanent contract) | Last 3 months |

| Weekly paid | Last 8–13 weeks |

| Variable income (commission/overtime) | Up to 6 months + employer letter |

| Zero-hours or temporary contract | Up to 12 months |

| New job (less than 3 months in role) | Offer letter + available payslips |

UK brokers are not just checking the number, they are checking for consistency. If your income fluctuates significantly from month to month, expect more questions. If you have recently received a pay rise, changed jobs, or started receiving bonus income, let your broker or lender know upfront. Some lenders include bonus income fully; others only count 50%.

Important note: Your payslips must clearly show your full name (matching your ID), your employer’s name, your pay date, your gross and net pay, and your year to date totals. Screenshots from a phone screen are usually not accepted, PDF downloads from your payroll portal are preferred.

Documents Needed for Employed Applicants

- Last 3 months’ payslips (or more, depending on contract type).

- Most recent P60.

- Last 3–6 months’ bank statements.

- Proof of identity (passport or UK driving licence).

- Proof of address (utility bill, council tax letter, or bank statement dated within 3 months).

- Proof of deposit (savings account statements showing the deposit has been building over time).

Documents Needed for Self-Employed Applicants

Self-employed applicants are not at a disadvantage when it comes to getting a mortgage but they do need to provide a more detailed picture of their income.

| Self-Employment Type | Documents Required |

| Sole trader | Last 2–3 years’ SA302s and Tax Year Overviews from HMRC |

| Limited company director | Last 2 years’ accounts + salary and dividend vouchers |

| Contractor/freelancer | Contracts, SA302s, and sometimes 6–12 months’ business bank statements |

| Partnership | Share of net profit for last 2 years |

Most lenders want at least 2 years of trading history for self-employed applicants. Some specialist lenders will consider applications with just one year of accounts, particularly if income has been growing steadily. This is where a whole-of-market mortgage broker adds genuine value, they know which lenders are flexible on this.

Proof of Deposit: What Brokers Want to See

Your deposit needs a clear paper trail. Brokers want to see that the money is yours, that it has been in your account for some time (typically at least three months), and that it did not arrive as a disguised loan.

- Savings: Bank statements showing the deposit building over time.

- Gifted deposit: A signed gift letter from the donor confirming the money is a gift, not a loan, and that they have no claim on the property. Close family gifts are standard; gifts from friends or distant relatives face additional scrutiny.

- Inheritance: Probate documents and bank statements showing the funds landing in your account.

- Property sale: Completion statement from your solicitor.

Large deposits that appear suddenly, particularly from overseas accounts, will trigger further questions. This is not a red flag in itself, but you need to be prepared to explain and evidence the source.

Step 4: What Do Mortgage Brokers Look for on Bank Statements?

This is one of the most searched and least thoroughly answered questions in the mortgage space. Most articles mention “gambling and overdrafts” and move on. Here is what lenders actually look at and what each thing signals to an underwriter.

How Many Months of Bank Statements Do You Need?

| Applicant Type | Statements Required |

| Employed (standard) | 3 months |

| Employed (variable income) | 3–6 months |

| Self-employed | 6–12 months (personal and business) |

| First-time buyer | Often 6 months to evidence savings discipline |

Most lenders now accept PDF bank statements downloaded from your online banking. However, some still require original hard copies posted directly from your bank. Your mortgage broker will advise on what your specific lender requires.

What Lenders Actually Check Line by Line?

| What They Look At | What They Want to See | What Raises Concerns |

| Salary deposits | Regular, consistent, matching declared income | Income that does not match application figures |

| Regular outgoings | Bills, subscriptions, loan payments | Undisclosed debts or commitments |

| Overdraft usage | Occasional, short-term use | Regularly maxing out the overdraft each month |

| Gambling transactions | Absent or minimal | Frequent or high-value betting activity |

| Buy-now-pay-later (BNPL) | Disclosed and manageable | Undisclosed BNPL commitments that affect affordability |

| Large unexplained deposits | Source identified and documented | Sudden lump sums with no paper trail |

| Returned direct debits | Not present | Failed payments suggest budget is under strain |

| Overseas transfers | Explained and evidenced | Unexplained international payments |

Red Flags That Can Affect Your Mortgage Application

Payday loans are one of the most serious red flags on a bank statement. Even if fully repaid, many lenders will decline or significantly limit lending to anyone who has used a payday loan in the past 12 to 24 months. It signals financial distress in a way that other borrowing does not.

Frequent overdraft use is less severe but still problematic. Dipping into an arranged overdraft occasionally is unlikely to cause issues. Regularly sitting at your overdraft limit suggests your income is not comfortably covering your outgoings, which makes lenders nervous about adding a monthly mortgage payment on top.

Gambling transactions are reviewed in context. Small, infrequent bets are unlikely to cause a problem. Regular or high value gambling activity is a different matter, it suggests unpredictable financial behaviour and can result in decline, even from applicants who are otherwise strong candidates.

Undisclosed debts if your bank statement shows a loan repayment or subscription that you did not declare in your application, underwriters will question it. Even small discrepancies between what you declared and what shows on your statements can trigger further investigation.

How to Clean Up Your Bank Statements Before Applying?

This is practical advice that almost no top ranking page offers in any useful detail. If you are planning to apply for a mortgage in the next three to six months:

- Stop using your overdraft or, at a minimum, reduce usage significantly so it does not appear on the statements lenders will review.

- Cancel subscriptions you do not use; it reduces visible outgoings and improves your affordability calculation.

- Avoid BNPL purchases in the run up to your application, these are increasingly visible to lenders and reduce your apparent disposable income.

- Reduce or stop gambling transactions for at least 3 months before applying.

- Do not make large cash withdrawals without a clear reason, unexplained cash movements raise anti money laundering flags.

- Keep your income going into the same account; lenders want to see a clean, consistent income trail in one place.

- Save consistently, even in small amounts. Regular monthly transfers to a savings account demonstrate financial discipline, which lenders actively look for.

Step 5: Submit Your Full Mortgage Application

Once you have an accepted offer on a property and your documents are ready, you submit your full mortgage application. This is the stage where everything you have prepared gets formally assessed.

Should You Use a Mortgage Broker or Apply Direct?

Both routes are valid, but using a whole of market mortgage broker gives you access to deals that are not available directly to the public, saves you significant research time, and means a qualified adviser, usually holding a CeMAP qualification and regulated by the Financial Conduct Authority (FCA), is handling your application.

Brokers also know which lenders are likely to approve your specific circumstances, which matters particularly if you are self employed, have a complex income structure, or have had credit issues in the past. Applying to the wrong lender and getting declined leaves a mark on your credit file.

What Happens During Mortgage Underwriting?

After your application is submitted, the lender’s underwriting team conducts a detailed assessment. They are not just checking your numbers, they are stress testing your ability to repay.

The mortgage affordability stress test checks whether you could still afford your monthly repayments if interest rates were to rise. This is a regulatory requirement and applies regardless of whether you are on a fixed or variable rate.

Underwriters will also check:

- That your declared income matches what your payslips and bank statements show.

- That all financial commitments have been disclosed.

- That the source of your deposit is legitimate and documented.

- Whether there are any other risk signals in your financial profile.

This stage can involve back and forth between your broker or solicitor and the lender. Stay responsive, delays at underwriting are often caused by slow responses to additional information requests.

Step 6: Property Valuation

Once underwriting is underway, the lender instructs a surveyor to carry out a property valuation. This confirms that the property is worth at least what you are paying for it and is suitable security for the loan.

Types of Property Surveys in the UK

| Survey Type | What It Covers | Typical Cost |

| Basic lender valuation | Confirms value for mortgage purposes only | Often free or included in product |

| RICS Homebuyer’s Report | Condition assessment plus valuation | £400–£1,000 |

| Full structural survey | Detailed inspection including structure | £600–£1,500+ |

The lender’s basic valuation protects the lender, not you. For older properties, those with unusual construction, or anything you plan to renovate, a full structural survey is strongly recommended.

What if the Valuation Comes Back Low?

A down-valuation, where the surveyor values the property below the agreed purchase price, is more common than most buyers expect. If this happens, you have a few options:

- Renegotiate the purchase price with the seller.

- Make up the difference with additional funds from savings.

- Challenge the valuation through your broker, who may be able to request a review or approach a lender with a more favourable valuation approach.

- Walk away with a down valuation gives you legitimate grounds to withdraw from a purchase.

Step 7: Receive Your Mortgage Offer

Once underwriting and valuation are both satisfactory, the lender issues a formal mortgage offer. This is a legally binding document outlining the exact terms of your mortgage, the amount, interest rate, term, monthly repayments, and any conditions.

What to Check Before Accepting a Mortgage Offer?

Do not assume the mortgage offer matches what you discussed. Before signing:

- Check the interest rate; confirm it matches the product you applied for.

- Check the mortgage term; 25 years is common but not automatic.

- Review early repayment charges (ERCs); understand the penalty if you want to leave the deal early.

- Check portability; can you take this mortgage to a new property if you move before the term ends?

- Note any special conditions; some offers are conditional on work being done to the property.

You typically have 7 days to review the offer before you are required to act, though in practice most lenders will allow longer.

How Long is a Mortgage Offer Valid?

Most UK mortgage offers are valid for 6 months from the date of issue. If your purchase does not complete within this window due to solicitor delays, chain issues, or other complications, you will need to request an extension from the lender. Most lenders will grant this, but it is not guaranteed, and in some cases you may need to reapply.

This is something almost no top companies mention, but it matters enormously to buyers in slow moving chains.

Step 8: Conveyancing, Exchange & Completion

Once your mortgage offer is in place, your solicitor takes over the legal side of the purchase. This stage is called conveyancing.

What Your Solicitor Does

Your solicitor or licensed conveyancer carries out property searches, reviews the contract of sale, manages the transfer of funds, and handles the legal registration of your ownership. Choosing an experienced property solicitor, not just the cheapest option, makes a significant difference to how smoothly this stage goes.

Note: Solicitor fees for buying a house usually range from £1,000 to £2,500 depending on the property value and the complexity of the transaction. This is separate from disbursements, the third party costs your solicitor pays on your behalf, such as Land Registry fees, local authority searches, and stamp duty.

What are the Additional Costs of Buying a Home?

Many first-time buyers budget only for their deposit and forget about the other costs involved. Here is a realistic breakdown:

| Cost | Estimated Amount |

| Solicitor/conveyancer fees | £1,000–£2,500 |

| Stamp Duty Land Tax (SDLT) | £0 for first-time buyers up to £425,000 |

| Property survey | £300–£1,500 |

| Mortgage arrangement fee | £0–£2,000 (sometimes added to mortgage) |

| Mortgage broker fee | £0–£500 (many charge nothing) |

| Building insurance | £150–£400/year (required from exchange) |

| Moving costs | £300–£1,500+ |

| Land Registry fee | £45–£500 depending on property value |

Exchange and Completion

Exchange of contracts is the point at which the sale becomes legally binding. Both buyer and seller sign the contracts, and the buyer pays their deposit to the solicitor. If either party pulls out after the exchange, financial penalties apply.

Completion is the day the mortgage funds are transferred, ownership changes hands, and you collect your keys. This is the moment the entire process has been building toward.

Common Mistakes to Avoid During the Mortgage Application Process

Dos and Don’ts Before and During Your Application

| DO | DON’T |

| Check your credit report at least 3 months before applying | Apply for new credit cards, car finance, or loans |

| Gather all documents before you start | Change jobs mid-application without telling your broker |

| Get an Agreement in Principle before viewing properties | Make large unexplained cash deposits |

| Use a whole-of-market mortgage broker | Use a payday loan in the 12–24 months before applying |

| Tell your lender about all income and financial commitments | Apply to multiple lenders simultaneously |

| Keep your income going into one consistent bank account | Make large purchases (car, holiday) before completion |

| Save consistently and avoid draining your deposit account | Ignore your solicitor’s requests for information |

| Build in time for delays — especially in a chain | Assume the process will take the minimum time |

Mortgage Application for Special Circumstances

The standard mortgage application process works well for employed applicants with simple income and credit histories. But many buyers fall outside that bracket and the process is still very much achievable.

Getting a Mortgage After a Job Change

Changing jobs just before or during a mortgage application is one of the most common triggers for delays or declines. Lenders prefer applicants who can demonstrate employment stability. If you have recently changed jobs, you may be required to have completed a probationary period before some lenders will consider your application. Others will accept an offer letter and a first payslip.

If your new role is in the same industry at the same or higher salary, the impact is much lower. If it is a career change with a variable income structure, moving from a salary to self-employment, for example, expect a more detailed assessment.

Getting a Mortgage on Maternity or Paternity Leave

Being on parental leave does not disqualify you from getting a mortgage. Lenders are required to consider your income on the same basis as any other applicant. However, they will typically want a letter from your employer confirming your return-to-work date and your expected salary when you return. Your broker should present your application carefully to lenders who handle parental leave applicants fairly.

Getting a Mortgage with a Poor Credit History

A poor credit history does not automatically mean no mortgage. It does mean you will need a specialist lender, a larger deposit, and in most cases, the help of an experienced mortgage broker who knows the adverse credit market.

The key factors lenders look at are: how serious the credit issues were, how long ago they occurred, and what your credit behaviour has looked like since. A missed utility bill two years ago is very different from a CCJ or a repossession.

Some lenders specialise in applicants with defaults, CCJs, or discharged bankruptcies. Rates will be higher, but the mortgage is achievable and remortgaging onto a better rate once your credit profile has improved is a realistic medium-term plan.

Getting a Mortgage as a First-Time Buyer

First-time buyers have access to some specific advantages in the UK mortgage market. Beyond the stamp duty relief on properties up to £425,000, there are government-backed schemes worth exploring, including the Mortgage Guarantee Scheme, which supports 95% LTV lending.

Buy-to-let mortgages are generally not available to first-time buyers, most lenders require you to own a residential property before they will consider a buy-to-let mortgage application. If you are considering the buy-to-let route as a first step onto the property ladder, specialist advice is essential. Use a buy-to-let mortgage calculator to understand realistic rental yield requirements before committing.

Final Thoughts

The UK mortgage application process has a lot of moving parts, but none of them is beyond reach with the right preparation. Start with your finances, get your documents in order before you need them, understand what lenders are actually looking for and do not underestimate the value of working with a qualified, whole-of-market mortgage broker who can match your specific circumstances to the right lender from the start.

The difference between a smooth four-week application and a three-month ordeal almost always comes down to preparation. The borrowers who sail through are not the ones with the highest salaries, they are the ones who turned up ready.

FAQs

How long does a mortgage application take in the UK?

From full application to formal mortgage offer, typically 4 to 6 weeks. The complete process from initial enquiry to completion is usually 2 to 6 months, depending on the chain and solicitors involved.

How many payslips do I need for a mortgage?

Most lenders require your last three monthly payslips if you are paid monthly. Weekly paid workers may need up to 13 weeks of payslips. Self-employed applicants do not use payslips, they need SA302s and Tax Year Overviews instead.

What do mortgage lenders look for on bank statements?

Lenders check income consistency, outgoings, overdraft usage, gambling transactions, undisclosed debts, and the source of your deposit. They are looking for evidence that you manage your finances responsibly and that your declared income matches what they can see on paper.

Does getting a mortgage in principle affect my credit score?

An AIP that uses a soft credit search does not affect your score. Some lenders use a hard search for an AIP, this will leave a mark on your credit file. Always check which type of search a lender performs before proceeding.

What credit score do I need for a mortgage in the UK?

There is no universal minimum. Each lender has its own thresholds, and they each use different credit reference agencies. A good credit score on Experian is 881 or above; on Equifax, 420 or above. The stronger your score, the more options you have and the better the rates available to you.

Do first-time buyers pay stamp duty?

First-time buyers in England and Northern Ireland pay no stamp duty on properties up to £425,000. Between £425,001 and £625,000, a 5% rate applies on the portion above £425,000. Properties above £625,000 are subject to standard stamp duty rates with no first-time buyer relief. Rules differ in Scotland (Land and Buildings Transaction Tax) and Wales (Land Transaction Tax).

What happens if my mortgage application is declined?

Do not apply elsewhere immediately. Multiple hard credit searches in quick succession damage your credit score further. Speak to a whole-of-market broker, understand why the application was declined, and address the issue before approaching another lender.

How long is a mortgage offer valid?

Most mortgage offers are valid for 6 months. If your purchase is delayed beyond this, contact your lender to request an extension. Most will accommodate this, but it is not guaranteed.

What is the difference between a mortgage offer and a mortgage in principle?

A mortgage in principle is a preliminary indication of how much a lender may be willing to lend, based on limited information and without a full assessment. A formal mortgage offer is issued after full underwriting, valuation, and affordability checks and it is the binding commitment from the lender to fund your purchase.

Can I overpay my mortgage?

Most mortgage products allow overpayments of up to 10% of the outstanding balance per year without triggering an early repayment charge. Overpaying reduces your outstanding balance, cuts the total interest you pay, and can shorten your mortgage term significantly. Use a mortgage overpayment calculator to see exactly how much you could save.