Table of Contents

ToggleIf your current mortgage deal is ending soon, you have probably started hearing the word “remortgage” quite a lot. At first, it can sound a bit confusing. But actually, remortgaging is pretty simple once someone explains it in simple words.

In the UK, many homeowners remortgage to save money, get a better interest rate, borrow extra funds, or switch to a mortgage that suits their current situation better. By the way, with mortgage rates changing over the past few years, more people now compare deals earlier instead of waiting until the last minute.

Basically, remortgaging means replacing your existing mortgage with a new one. You can stay with the same lender or move to a different mortgage provider. The main goal is usually to improve your financial situation or avoid paying a higher standard variable rate (SVR).

The good thing is that the process is often easier than taking out your first mortgage. You already own the property, so lenders mainly check your income, affordability, credit history, and the current value of your home.

In this guide, we will explain:

- What remortgaging means.

- Why people remortgage.

- When it makes sense to remortgage.

- How the remortgage process works.

- What costs you need to know about.

- How BM14 Finance helps you compare suitable deals.

So, if you are wondering how does remortgaging work in the UK, this guide breaks everything down in a simple and practical way.

What is a Remortgage? / What Does Remortgage Mean?

A remortgage happens when you move your current mortgage to a new deal. This can happen with:

- Your existing lender.

- A completely different lender.

For example, let’s say your fixed-rate mortgage ends next month. If you do nothing, your lender may move you onto their standard variable rate. Usually, that rate costs more each month.

Instead, you can remortgage onto a new deal with a lower interest rate or better terms.

Pretty sure this is one of the main reasons many UK homeowners start looking at remortgage deals around 3 to 6 months before their current deal ends.

A remortgage can help you:

- Lower monthly payments.

- Borrow more money.

- Change mortgage types.

- Reduce long-term interest costs.

- Consolidate debts in some cases.

Of course, every situation is different. Some people remortgage for savings, while others want more flexibility.

Why Do People Remortgage?

People remortgage for many different reasons. In some cases, homeowners want a lower rate. In other situations, they need extra borrowing for home improvements, debt consolidation, or major life changes.

Eventually, your financial situation changes over time. Your income may increase, your property value may rise, or your mortgage deal may stop being competitive.

Here are some of the most common reasons to remortgage, as well as the benefits of remortgaging your home:

My Current Mortgage Rate is Coming to an End

This is one of the biggest reasons people remortgage in the UK.

Most mortgage deals come with:

- Fixed rates

- Tracker rates

- Discount rates

These deals usually last between 2 and 5 years. Once the deal ends, lenders often move borrowers onto the standard variable rate.

The problem is that SVR rates are usually higher. That means your monthly repayments can rise quite quickly.

For example:

- You may currently pay 4.5%

- Your lender’s SVR may jump to 7% or more

That difference can add hundreds of pounds to your monthly payments over time.

Basically, remortgaging before your current deal ends helps you lock in a better rate and avoid unnecessary costs.

I Want to Remortgage When My House Value Has Increased

If your property value has gone up, remortgaging could work in your favour.

Lenders look at your loan to value ratio (LTV). This compares:

- Your mortgage balance

- Your property value

For example:

- Your home was worth £220,000

- It is now worth £280,000

As your equity increases, lenders may offer better remortgage rates because you appear less risky as a borrower.

Actually, many UK homeowners remortgage after:

- Renovations.

- Extensions.

- Loft conversions.

- Local property price growth.

A lower LTV opens the door to cheaper mortgage products.

I Want to Switch From Interest Only to a Repayment Mortgage

Some borrowers originally choose an interest only mortgage because the monthly payments are lower.

However, with an interest only mortgage:

- You only pay the interest

- The original loan balance stays the same

Eventually, many homeowners prefer switching to a repayment mortgage. With repayment mortgages:

- You pay interest

- You gradually pay off the actual loan

This means you slowly build ownership in your property over time.

By the way, some people switch because they want more financial security before retirement.

I Want to Get a Better Interest Rate

Mortgage rates change regularly in the UK market.

If rates drop or your financial position improves, you may qualify for a better deal than the one you currently have.

Even a small drop in interest rates can make a noticeable difference over the full mortgage term.

For example:

- A lower rate may reduce monthly payments

- You may save thousands in long-term interest

That is why many borrowers compare remortgage deals regularly instead of staying on the same mortgage for years.

I Want to Make Overpayments on My Mortgage

Some mortgage products limit how much extra you can pay each year.

If you now want more flexibility, remortgaging could help you move onto a mortgage with friendlier overpayment terms.

Making overpayments helps:

- Reduce your mortgage balance faster

- Cut overall interest costs

- Shorten your mortgage term

Quite a few homeowners do this after:

- Salary increases

- Receiving bonuses

- Inheriting money

- Reducing other debts

I Want to Borrow More Money on My Mortgage

Many homeowners remortgage to release equity from their property.

This means borrowing extra funds against the value of your home.

People often use this money for:

- Home improvements

- Extensions

- Debt consolidation

- Buying another property

- Family expenses

For example, improving your kitchen or adding an extra bedroom may also increase your property’s value in the long run.

Still, borrowing more increases your mortgage debt, so it is important to check affordability carefully.

Is it Time to Remortgage?

A lot of homeowners ask this question when their current deal starts nearing the end.

Usually, it is worth reviewing your mortgage if:

- Your fixed deal ends within 6 months

- Your interest rate looks expensive

- Your property value has increased

- Your financial situation has improved

- You want lower monthly repayments

- You need extra borrowing

On the other hand, sometimes remortgaging too early can trigger early repayment charges.

That is why timing matters quite a lot.

Basically, reviewing your mortgage early gives you more time to:

- Compare lenders

- Review rates

- Prepare documents

- Improve your credit profile if needed

Get Ready to Remortgage

Before starting a remortgage application, it helps to organise your finances properly.

Lenders normally check:

- Your income

- Employment details

- Credit history

- Existing debts

- Monthly spending

- Property value

Getting these things ready early can speed up the process.

At BM14 Finance, borrowers can explore different mortgage and insurance options based on their situation. Working with mortgage advisors helps people understand:

- Fixed-rate mortgages

- Variable rates

- Loan-to-value bands

- Affordability rules

- Early repayment charges

Quite honestly, many people find mortgage paperwork stressful at first. But once the documents are prepared properly, the process becomes much smoother.

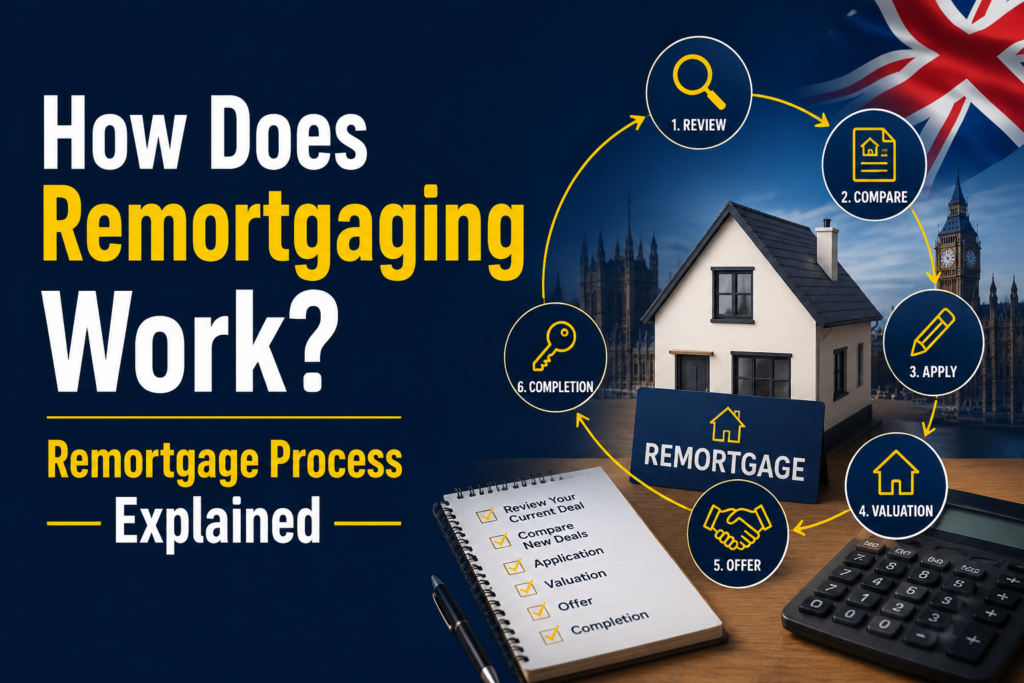

How the Remortgage Process Works?

The remortgage process usually follows a few simple stages. While every lender works slightly differently, most UK remortgages follow a similar path.

Complete an Agreement in Principle

An Agreement in Principle (AIP) gives you an early idea of how much a lender may lend you.

The lender performs:

- A basic affordability check

- A credit review

This stage does not fully approve the mortgage, but it helps you understand your borrowing position.

An AIP also helps mortgage advisors narrow down suitable remortgage deals faster.

Consider All the Costs

Remortgaging is not only about interest rates.

You should also check:

- Arrangement fees

- Valuation fees

- Legal fees

- Broker fees

- Early repayment charges

Sometimes a lower rate may still cost more overall because of higher fees.

Basically, always compare the total cost of the mortgage instead of focusing only on the headline rate.

Apply for Your New Mortgage

Once you choose a lender, you complete the full application.

The lender may ask for:

- Payslips

- Bank statements

- ID documents

- Proof of address

- Tax calculations for self-employed applicants

They also review your property value and affordability in more detail.

If everything looks good, the lender issues a formal mortgage offer.

Completing Your Remortgage

After approval, solicitors handle the legal side of the remortgage.

The new lender then:

- Pays off your old mortgage

- Transfers the new mortgage onto your property

Once completed, your new mortgage deal officially begins.

Actually, many easy remortgages are completed within several weeks, although timings vary depending on:

- The lender

- Legal work

- Property checks

- Financial circumstances

How to Remortgage?

If you are planning to remortgage soon, these steps make the process easier to understand.

Find Out What Your Property is Worth?

Your property value plays a major role in the rates available to you.

You can:

- Use online valuation tools

- Compare local property sales

- Request a professional valuation

A higher property value may improve your loan to value ratio and unlock better mortgage deals.

Check How Much is Left to Pay

Before comparing deals, review:

- Your remaining mortgage balance

- Your current interest rate

- Remaining mortgage term

- Early repayment charges

This helps you calculate whether remortgaging makes financial sense.

Apply for an Agreement in Principle (AIP)

An AIP helps show what lenders may lend you based on your financial situation.

It also helps identify possible issues early, especially if:

- You are self-employed.

- Your income changed recently.

- Your credit history needs improvement.

Compare Our Remortgage Rates and Deals

Comparing lenders carefully matters quite a lot in today’s mortgage market.

You should review:

- Fixed-rate mortgages

- Tracker mortgages

- Product fees

- Flexibility

- Overpayment options

At BM14 Finance, borrowers can compare mortgage and insurance options based on their financial goals and circumstances.

Pretty often, getting professional guidance helps borrowers understand which mortgage suits them best instead of choosing the lowest advertised rate.

Check All Remortgage Costs

Some remortgage products come with:

- Free valuations

- Free legal work

- Cashback incentives

Others may include higher fees.

That is why it helps to review:

- Total borrowing costs

- Monthly payments

- Long term interest costs

Eventually, the cheapest looking rate does not always become the cheapest mortgage overall.

Apply for Your Mortgage

Once you choose your deal, the lender completes the final checks.

At this stage:

- Your documents are reviewed completely

- Affordability gets confirmed

- The property valuation is complete

If approved, the lender sends your official mortgage offer.

Final Step for Completing a Remortgage

Your solicitor or conveyancer handles the final legal process.

The new mortgage lender pays off the existing mortgage balance, and your new deal starts immediately afterwards.

From that point, you simply begin making payments under your new mortgage agreement.

Final Thoughts

So, how does remortgaging work?

In simple words, remortgaging means replacing your current mortgage with a new deal that better suits your needs. People remortgage for many reasons, including:

- Lower interest rates

- Better mortgage terms

- Borrowing extra money

- Switching mortgage types

- Reducing monthly payments

The good news is that the process is usually more simple than many people expect.

Still, timing matters quite a lot. Reviewing your mortgage before your current deal ends can help you avoid higher rates and unnecessary costs.

By the way, every borrower’s situation looks different. That is why comparing deals carefully and understanding all fees becomes important before making any decision.If you are thinking about remortgaging, discussing with experienced mortgage advisors like BM14 Finance helps you explore suitable remortgage and insurance options based on your financial goals.